Once a month - at around about this time (approximately 3 working days until the start of a new calendar month) - me and Ms.79 set aside a couple of hours to do all of our bill reviews, bill payments, money-in-the-bank-optimisations and other ad-hoc finance-related things. All of this is done on-line - and can sometimes be quite a chore and almost always involves some tricky juggling acts. Let me explain …

Ever since we bought our current home nearly two years ago - we decided to open up one of those “debt” bank accounts to service the mortgage. This is the type of account that is an alternative to your conventional mortgage repayment account in the sense that it is a universal account for all our “money in” and all our “money out” - and since the largest “money out” item that we had on the account when we opened it around 2 years ago was the mortgage advance for our house purchase, the account shows that we are constantly in debt - although that debt is constantly being eroded by “money in” salary payments and other ad-hoc bits of income. There are many different banks which do accounts like this - but we use Virgin One. The problem is that for one reason or another which I won’t go into here - only my salary gets paid into that account. Ms.79 has a separate account with an Internet bank called Smile for her salary - and we also have a joint account with Halifax which is where we both used to have our salary paid - but we now just use for some direct debits that we cannot easily find ways of moving - and for petty cash withdrawals funded by monthly top-ups from our other accounts. I also have credit cards from Barclaycard and a chargecard from Diners Club. Every month we review our bills and pay off any that aren’t paid automatically - e.g. credit cards and ad-hoc bills - and every month we play a careful game of rebalancing our accounts so that the maximum possible is used to erode the debt in the mortgage account without leaving us dangerously “non-liquid”.

The “juggling act” that I referred to earlier is not so much to do with the movement of money described above - but more to do with the fact that we generally have to huddle around my laptop and log-in to around 5 or 6 different websites all at the same time: banks, credit-cards, service providers etc. Each site has a completely different type of secure sign-in procedure which involve various combinations of username, id numbers, pin-codes, passwords, memorable names, memorable dates, security phrases, key codes etc. and each involves different (and often randomised) challenges to different digits or characters of some of those codes. We normally store all of our “precious” authorisation credentials in a very-high-bit-length encrypted database on a separate personal organiser that we carry around with us - so logging into all these websites involves cross-referencing with the data in our encrypted database - so lots of switching between tiny personal organiser screen and keyboard and the laptop screen and keyboard as we are huddled there. And you have to act FAST - because by the time you have got to signing in to the last website - the first one might have expired its “security timeout”! And we often have to constantly randomly switch between windows to randomly press some keys and click some links - just so that we can keep the websites “alive” so that they don’t expire on us whilst we’re busy analysing or performing actions on our money and bills.

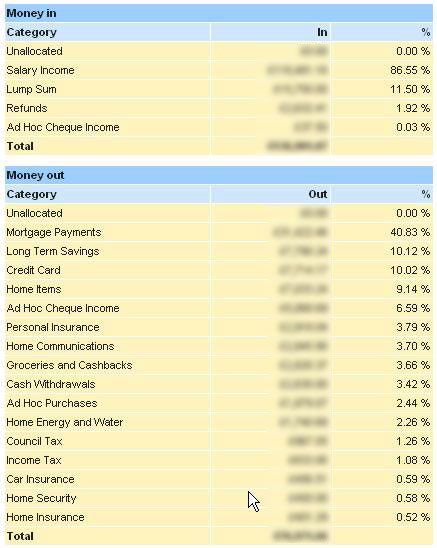

Anyway - the really smart thing about the Virgin One online banking facility is that you can categorise your “money in” and “money-out” with user-defined labels. And then you can produce reports and analyses of your spending patterns and incomes. I’ve never used that facility before because I’ve never had a substantial amount of prehistoric data of transactions in my account for the reports to be of any use - due to my account being fairly new - but this time I figured that I’ve had the account for nearly two years - so it might be worth generating some reports. And here is the most interesting report of our incomings and outgoings as per the categories that I defined. I have blurred out the actual values so that you don’t laugh at how little money we have to play with - but the percentages are intact, and this is what makes the analysis fascinating:

Where my money has gone in the last 2 years

Some questions that I would really love to know answers for are:

- Is 40% of spend (not income) on mortgage typical for a UK person? I wonder how this compares for people in other countries?

- Is 10% of spend (not income) on long-term savings typical?

- Is 27% of spend (not income) on non-groceries (e.g. home items, clothes, gadgets, gifts, holiday stuff etc.) typical?

- Is 7% of spend (not income) on groceries and other cash-related consumables (e.g. lunch money etc.) typical?

- Is 9% of spend (not income) on home utility (i.e. Internet, satellite TV, energy, water, home insurance, car insurance, security, Council Tax) typical?

- Is 4% of spend (not income) on life insurance and income protection typical?

Posted by jag at December 29, 2003 06:42 AM“Money: get back

I’m all right Jack

Keep your hands off my stack.“

From a song called “Money” by Pink Floyd

40% on mortgage seems a bit too high.…. (though I dont know much about mortgage amounts in UK, for that matter, anywhere).

But I am not in a position to comment on that. Its your way of organising money flows

Evening Jag,

it seems like I need you not only to come around and sort out my finances, but also network my computers and run my website. A bit of ironing wouldn’t go amiss either.

But seriously, I’ve never analysed my income in that depth but it could be a useful exercise. What I can add from my perspective in Munich is that I pay rent, as most here do, and that accounts for ca. 50% of my post-tax income. That’s high, but Munich is astronomical, although it could be a common figure. The funny thing is how easy it is to slip from comfort to penny-pinching: we have three kids any my wife doesn’t work. Imagine 30% less rent, no children, and double income. That was our state around 8 or 9 years ago and it was a good life. Now we adore the kids (mostly? frequently?) but we sure as hell miss the comfort of that spare cash. To be honest: we didn’t see the change coming.

David

Sat: Well I’ve just read somewhere that (in UK at least) you should budget for no moe than 30% of income on mortgage. My 40% of spend on mortgage is actually just less than 30% of my income - which means that I am probably in “the norm” for here in UK.

David: Yes - you have reminded me that Germany is not a country of “owner-occupiers” - and that most people rent. I also can empathise with your situation in Munich - as I have some friends who live there and suffer same high-rent problem.

I can see what you mean about kids - and if I read the sentiment correctly - they’re worth every minute and sacrificed penny of it! (I have two myself 8 and 5). Strangely for us - we are more comfortable now than we were before kids - and that’s probably due to several career changes (for the better) since before the kids arrived. And also Ms.79 works now too - so that helps a great deal - as well as relieving the boredom given that the little ones are out at school all day these days!

Posted by: Jag on December 31, 2003 01:42 PMhow very organised! I suspect I spend more than 40% on mortgage - at least now that I work from home and don’t spend much other than basic bills. Not having a car makes a big difference for me. In the states, a big proportion would be spent on car payments and fuel, not to mention the insurance…

Posted by: Lisa on January 1, 2004 01:38 PMI don’t think I am at all typical of people living in the U.S., but my expenses break down as follows (not as accurately tabulated as yours, but more or less correct):

rent 39.7

food 22.7

utility bills 14

household 5.8

art supplies 5.5

transportation 4.5

miscellaneous 3.2

internet 2.5

toiletries 2.1

If some of these seem high (5.5% spent on art supplies?), it’s because my total expenditures are only about $600 U.S. dollars a month.

So very organised Jag.

I wd have to consult my accountant (hehe… its my wife) who, am sure would hav done a similar analysis.

Lisa/Chakra: I’m actually very disorganised when it comes to money. And Ms79 is the same. That’s why we like online banking - the website just prompts me to categorise the expense - and it produces the reports for me!

Lisa: I see what you mean about the car. I’ve only ever bought used cars (under 2500 pounds) so I’ve never had car-payments as such. And at that sort of price - insurance is cheap. Also - living in London/UK (high fuel prices and plenty public transport) means that we only use car when public transport would actually be inconvenient.

asfo_del: thx for commenting here - and sharing your expense breakdown. Fascinating. Yes - it seems that you are not typical - $600 a month is virtually £300 ! I’m impressed!

Posted by: Jag on January 3, 2004 12:14 PM